Today’s car of the day is Mr A’s classic Austin Mini GT.

Mr A’s Austin Mini GT has been insured with us here at AIB Insurance on a classic car policy meaning that his car is taken care of always. Agreed value is one of the many benefits that comes with a classic car policy as well as salvage retention.

Mr A also received a discount on this policy because of the length of ownership on this vehicle. If you also have a classic car that you have recently bought or have owned for a long period of time and would like to get a quotation call our specialist quotation team on 02380 268351.

If you also have photos of your classic car and would like to share them, email them to info@aib.co.uk. Thank you Mr A for sharing your photos!

The Triumph GT6 is a 6-cylinder fastback version of the Spitfire, styled by the Italian designer Giovanni Michelotti, and produced over 7 years from 1966 to 1973.

The 6-cylinder engine was tuned in the GT6 to develop 95 hp (71 kW) at 5000 rpm, and torque of 117 lb.ft at 3000 rpm. Its top speed was reported as being 106 mph and could accelerate from 0–60 mph in slightly under 12 seconds.

Mr G has his Triumph GT6 insured on a classic car policy here with us at AIB insurance. This means that Mr G has agreed value on his car as well as salvage retention.

Another benefit of the classic car policies is choice of repairer meaning that Mr G can choose where his car is taken and only have approved parts used on his car. If you have a classic car that you would like to have insured on this kind of policy, call our specialist team for a bespoke quote on 02380 268351.

If you have a classic car and would like to share your photos with us, email them into info@aib.co.uk.

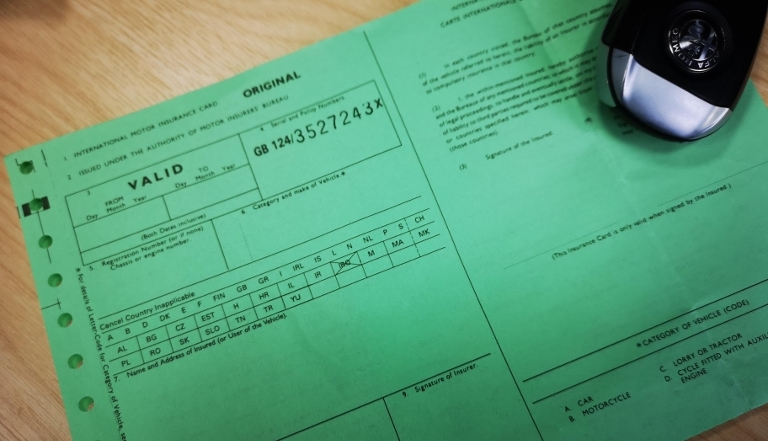

Ok, we know travelling abroad is still extremely limited. We also know some of you may be chomping at the bit to get away. To open up the engine of that brand new drop-top you impulsively purchased in a fit of lockdown excess and/or boredom! The lure of those long French roads, no other motorists in your mirrors for miles… azure waters lapping at the edges of ocean drives… wind in your hair, freedom at your pedals…

Well the whole process of taking your wheels abroad has just been made a whole lot easier. With a post Brexit boost for Blighty, it has been confirmed recently that the EU has ditched the car insurance green card. Drivers will no longer need to apply for this internationally recognised document confirming valid third party insurance, when travelling abroad to EU countries. The green cards were set to cause travel chaos for drivers looking to head across the continent as restrictions begin to ease.

Any driver without a card driving in the EU could have faced fines, prosecution or having their car impounded. However, the Commission decided to drop the card in an effort to reduce tension around the Northern Ireland protocol – a welcome change, making it easier for them to travel freely into the Republic of Ireland. The MIBI had protested against the cards, saying ‘It was not a sustainable solution, considering the estimated 43m cross border vehicle trips per annum”

Huw Evans, Director General at the Association of British Insurers said:

“This is excellent news. We have long campaigned for the UK to be part of the Green Card Free Circulation Zone so we warmly welcome the decision by the European Commission today. The Commission has taken a pragmatic approach on the matter. UK drivers will no longer need to apply for a green card through their insurer which will help reduce bureaucracy for drivers and road hauliers travelling between the UK and EU. It will be especially welcomed by motorists in Northern Ireland driving across the border to the Republic of Ireland.”

The move to remove the Green Card has been welcomed by the insurance industry who have campaigned to see an end to the practice.

Kirby De-Gray Birch, Director at Airsports Insurance Bureau, said:

‘It’s fantastic news and a sensible change although it still needs to be fully endorsed and rubber stamped by the European Union. Once fully approved though, this will make things a little less complicated for Britons who prefer to travel to Europe by road rather than flying there.

If you are travelling into the EU within the next three weeks we would encourage you to call us and order a green card if you haven’t already, but any travelers travelling after this date, hold tight until it’s all ratified.’

Be aware though, if you’re eagerly kitting out your camper for a road trip to remember, you will still need the document in place for the rest of this month. While the commission has confirmed it is ditching the card, the rules haven’t come into force just yet.

Until the EU has fully implemented the change, anyone taking their car to Europe will still need to get a Green Card from their insurer before they head off abroad to countries that require one. Post-change, your certificate of insurance will be enough to head out on the highway. Bon Voyage!

Winter is upon us and we have already seen temperatures fall below freezing on occasions here in the UK. Therefore, perhaps it is an appropriate time to mention about protecting your household pipes against the cold weather.

According to information published by the Association of British Insurers (ABI), you may find it rather concerning to read that the average amount of a burst pipe insurance claim due to adverse weather conditions exceeded £10,000 in 2018. This is a sizeable sum and a claim of such magnitude has no doubt caused a significant amount of damage whether it is to property, contents or both never mind the potential distress and upheaval to the owners of the premises.

The ABI has very kindly made some recommendations as to what action you can take to lower the possibility of your pipes getting frozen over the winter period: –

If you have one or more taps that drip when turned off get them repaired.

Check in the loft that any water tanks and water pipes are suitably insulated.

Make sure your heating is set to come on periodically even if you are away for a short break.

Make sure that you are familiar with where your stopcock is situated in your home.

If a pipe freezes then you should take the following action according to the ABI: –

Any contents such as clothes and furniture should be moved away from the pipes just in case one of the pipes bursts.

Do not try to remove ice using the likes of a blow torch or a hammer as this may damage the pipework even more.

Turn off the mains water at the stopcock until the pipes have defrosted.

If a pipe bursts, according to the ABI, you should: –

Remove any possessions to a safe place.

Turn off the stopcock, drain the water supply by turning on the taps, and turn off the water heating and central heating.

In the unfortunate event that you do suffer water damage, get in touch with your insurer as soon as possible.

With winter quickly approaching, the Association Of British Insurers (ABI) is recommending that both owners of homes and businesses make sure that there properties are in a good state of repair. This should help reduce the number of claims being made by people on their buildings and contents insurance policies here in the UK.

Apparently, on a daily basis, insurance companies pay out in the region of £14.3 million to owners of homes and businesses to meet claims from people in respect of replacing damaged content and carry out repairs due to adverse weather conditions resulting in properties suffering burst pipes and floods.

You may find the following suggestions made by the ABI of benefit to help ensure that your property is better able to cope with the ravages of winter: –

Arrange for your roof on your home or business premises to be checked to make sure that it is watertight and that there are definitely no loose or missing roof tiles. This sort of job is best left to a professional for safety reasons.

Find out where the stopcock is in the property and that it is working correctly.

Make sure that the gutters are free of debris and that they are not overflowing due to their being a blockage.

Check that the smoke alarm is working correctly.

Make sure that there are no visible damp patches in your property such as damage to a ceiling.

Make sure that water tanks in the loft and pipes are insulated.

Whilst it is not a legal requirement to have building and contents insurance in place covering your home and/or business premises as well as the contents and plant/machinery in them, it is a sensible course of action so that you can claim on such a policy when necessary.

In this respect, why not get in touch with a member of our team who has many years experience in arranging suitable, affordable cover who will be pleased to discuss your requirements and arrange for you to receive a competitive quotation without any obligation.

The Association of British Insurers (ABI) has recently published some interesting statistics relating to claims on motor insurance policies. Specifically, it has revealed that the average amount paid out last year for each motor insurance claim was the largest amount since records started to be kept for this sort of cover.

The figure was £2,936. Apparently, a couple of reasons why this sort of cover hit a record was down to the fact that the cost of repairing a motor vehicle has gone up as well as the amount paid out to meet claims when a car is stolen has risen which happens all too often.

Last year, a staggering £8.1 billion was paid out by insurers to meet all motor insurance claims. This was a similar figure to 2016. It would be potentially good news if the amount of such claims fell in 2018 and beyond as this is one of the many factors that affect how much insurance companies charge for their car insurance. Perhaps if the amount paid out for claims was to fall, we may see a reduction in the cost of our motor insurance policies.

Another interesting statistic is that the average amount paid out for a claim in respect of personal injury was £10,816 in quarter four of 2017. This is a large sum and is also a factor that dictates how much a motor insurance provider charges new and existing customers who renew their cover. Again, it would be lovely if we were to see the average amount paid out for a personal injury claim to drop as this is another factor that may impact on the amount motor insurance providers charge for their cover.

Apparently, the number of claims submitted for personal injury dropped slightly in 2017 when compared with 2016. Of the claims submitted, there were 320,000 that insurers agreed to pay out for.

Of course, policyholders would prefer not to have to be faced with having to claim on their car insurance policies but when they do it is important that they are confident that the insurance company the cover is arranged with will pay out in the event of a claim as quickly and effortlessly as possible. So, if you are looking for quality motor insurance that is not only competitively priced but also where the insurance company is well known for the number of claims that they agree to meet, then why not get in touch with us on 02380 268 351 and a member of our team will gladly do all that he or she can to assist.

If you want to arrange the likes of home (buildings and contents) insurance either for the first time or are considering moving your cover from your existing insurance company to a new provider there may be several factors that will have a bearing on which insurer you take out the cover with. For most people, the number one consideration is how much they will have to pay in premiums to the insurance company to protect their home and contents in the event of things like fire, flood, accidental damage and theft.

That may sound fine but the reason why you require such cover is to give you peace of mind so that if your home was burned to the ground, your Rolex stolen or your skiing equipment damaged in transit you could claim and the insurer would cover the vast majority of your claim to rebuild your property and/or replace or repair the damaged items. So, surely another factor that you should consider when deciding which insurer to arrange the cover with is the percentage of claims that it ends up paying out for.

In that respect, you may be interested to read that, on the 1st March 2018, the Financial Conduct Authority (FCA) published the “General Insurance value measures data – year ending 31 August 2017”. This document includes data from 36 insurance companies (UK and EEA firms) about claims acceptance rates, average claim pay-outs and claims frequencies. The publication can be viewed on the FCA’s website via the following link: –

If you take a look at the Claims Acceptance Rate column in the section relating to Home Insurance you will see that there is a wide variance in the percentage of claims insurers agree to pay out for.

At the top end of the scale the following insurers accepted 97.5% to 100% of claims: –

• Chubb European Group Limited

• Hiscox Insurance Company Limited

• Hiscox Syndicates Limited

• Acromas Insurance Company Limited

• Liberty Insurance Limited

• Royal and Sun Alliance Insurance PLC

• The Salvation Army General Insurance Company Limited

You will note that both Chubb and Hiscox are in the top scale of 97.5% to 100% when it comes to meeting claims. We are pleased to say that, here at AIB Insurance, they are two of the companies that feature highly on our panel of insurers when it comes to arranging buildings and contents insurance for our high net worth clients.

On the 25th January 2017, the first publication of the General Insurance value measures data – year ending 31 August 2016 was produced. On that day, James Bridge, Assistant Director, Head of Conduct Regulation, Association of British Insurers, said: “Every day home insurers pay out over £8 million in claims to customers, and are committed to doing all they can to ensure that insurance delivers when the worst happens. The FCA data shows that the vast majority of claims are paid out.”

When AIB Insurance recommends an insurance company to a client, we take several things into consideration such as price, claims experience and the quality of the customer service. So, if you are looking for home insurance or, indeed, any other insurance cover why not give us a call on 02380 268 351 to discuss your requirements with an experienced, friendly member of our team who will arrange to provide you with a competitive quotation. We look forward to being of assistance to you.

Over the past couple of years there has been an upward trend in the cost of insuring motor vehicles. This is possibly something that you have noticed when receiving your renewal notice and, if so, has hopefully triggered you to seek comparative quotations through the likes of ourselves to see if we can find you a better deal from another provider.

Well, the Association of British Insurers has recently produced the ABI Premium Tracker that monitors what the cost of motor insurance has been over an extended period of time. Apparently, the average premium paid for fully comprehensive cover throughout 2017 was £481 per annum. This was an increase of 9% in comparison to the cost 12 months ago that, in monetary terms, equated to a rise of £40 per annum.

Another disturbing statistic is the fact that the average cost of insuring a motor vehicle increased by a staggering 29% since back in 2014.

There are a number of factors that have caused this increase in the cost of motor insurance. For instance, repair costs of vehicles have gone up, there has been a rise in the number of people seeking compensation for whiplash injuries, Insurance Premium Tax has gone up and there has been a change in the calculation of compensation payouts.

The ABI is encouraging the Government to stop increasing the Insurance Premium Tax, make changes to how claims for lower value claims for whiplash are dealt with and also to look at the Ogden Discount Rate which is used to work out what compensation someone should receive who has suffered a significant injury as a result of a road traffic accident. These things are all with a view to potentially reducing how much someone pays for their motor insurance.

So, is there anything that you can do to mitigate such an increase? Well, you may wish to consider shopping around for cheaper cover but if you do, make sure that the level of cover meets your needs.

Here at AIB Insurance, we have been able to help arrange car insurance for a number of customers at a lower premium than their existing insurer has been charging them so why not give us a call on 02380 268 351 to discuss your requirements and obtain a quotation without any obligation.

Our clients may be interested to read that insurers here in the UK continue to pay out huge sums of money in respect of domestic claims for damage caused by water escape. In fact, it may come as a surprise to you to hear that such claims involve the biggest payouts for insurance companies providing this type of cover.

According to information provided by the Association of British Insurers (ABI), some £483 million was paid out by insurers for claims relating to the escape of water from domestic properties in the nine months from the 1st January to 30 September of this year. Unfortunately, that is a rise of 1% when compared with the first nine months of 2016. The average amount paid out by insurance companies for escaped domestic water damage is £2,638 per claim.

Such claims will no doubt include damage caused by people leaving taps on whilst filling up a bath thus leading to it overflowing and damaging both the upstairs and downstairs of a property. There will probably be numerous claims for water leakage from the likes of washing machines and dishwashers. As more homes have central heating systems fitted these days, damage caused by leakages from them is a factor as is greater use being made by the building industry of materials that are not as water resistant. More properties now have the likes of cloakrooms and en-suite bathrooms and en-suite shower rooms included in the design.

So, what can you do to reduce the likelihood of suffering such damage? Well, apart from making sure that taps are turned off after use, there are many things you can look at such as you should check the hoses on appliances such as washing machines to make sure that they are not leaking. If you have a hot water cylinder in your airing cupboard make sure that it is not leaking. Check that the toilet basins are not cracked. Make sure that radiators are not dripping water from the pipes that enter and come out of them as well as at the end of the top of the radiators where you occasionally let out the air. Also check the main stopcock that allows cold water into your home to establish that there are no drips coming from it. If you feel it is safe to do so, go up into the loft and make sure that the water tanks are not close to overflowing.

Do make sure that you have adequate buildings and contents cover in place so that, should you suffer water damage, you have the peace of mind of knowing that your claim will be speedily dealt with. In this respect, it is worth noting that here at AIB Insurance we have an extensive panel of insurers who are renowned for providing quality cover but also have an enviable reputation for processing claims. So, if you would like to receive a competitive quotation why not give us a call on 02380 268 351 and speak with a knowledgeable member of our team.

Here in the UK, we are sometimes faced with some stormy weather with high winds and flooding being a feature. Apparently, according to the Association of British Insurers (ABI), property insurance companies pay out on average £8.1 million pounds every day to meet claims for damage to homes and replace contents.

Below are some of the things that property owners could do to possibly reduce the level of damage that storms can cause to properties and their contents: –

• It would be a good idea to monitor the weather forecast so that, hopefully, you are not caught out by the arrival of a storm.

• If it is being forecast that strong winds are on their way then you should check that no items are left loosely in your garden or elsewhere outside that could be blown around thus potentially causing damage to those items, your property, pets and people. Wherever possible, either make sure that the loose items are securely tied down or bring them inside say into your garage and/or garden shed.

• Make sure that there do not appear to be any loose roof tiles.

• Loose branches can be blown away in a storm causing damage so you could get a tree surgeon to remove them.

• Make sure that fencing and the posts surrounding your garden are secure.

• If you are in an area that is susceptible to flooding then you may wish to have floodgates fitted or buy some sandbags to protect your home against the ingress of water. You may also wish to move items of furniture upstairs to protect them against water damage.

• In the event of you having to temporarily move upstairs due to flooding, you may wish to ensure that there is a supply of bottled water and food upstairs that can be consumed until you are rescued. You may also wish to have things like medicines, blankets and a torch to hand.

• You may wish to drive your car onto higher ground to avoid it being damaged by floodwater if it is safe to take this course of action. If there is no threat of flooding but there are strong winds forecast you may wish to put the car in the garage if this is an option available to you.

• Have available contact details for the likes of the gas and electric suppliers, water authority, local authority and buildings and contents insurance company.

• Check that your drains and guttering are not blocked.

• Make sure that your water tanks and pipes are insulated to provide protection in freezing weather.

We trust that you find the above of benefit.

Should you wish to receive a competitive quotation for buildings and/or contents cover then why not get in touch with us here at AIB Insurance on 02380 268 351 and a knowledgeable member of our team will be pleased to assist without any obligation on your part.

AIB Launch Classic Car Offering

AIB is proud to announce the launch of our non-standard per...

You must be logged in to post a comment.